Recently, Taktile Co-founder and CEO Maik Taro Wehmeyer sat down with AltFi and B2B lending experts Philip Kelvin (Co-founder and CEO at Tranch) and Nicolas Rabinovitch (Fraud and Credit Risk at Hokodo) to discuss how the emergence of B2B decision automation is unlocking new possibilities for lenders.

In case you missed it, we have recapped key takeaways from the discussion, which included:

- The benefits of automation in B2B lending

- Why alternative data sources are key to unlocking automation

- How AI can benefit B2B decision-making

- Getting started with automation

- How modern decision engines make automation simple

If you would like to learn in-depth about these topics, watch the full webinar

The benefits of automation in B2B lending

It is no secret that delivering an exceptional customer experience is key to growing a lending business. But to do this well, you must be able to provide offers at speed - something that, until recently, has not been characteristic of the B2B lending industry.

Now, we are seeing the emergence of sophisticated B2B fintechs taking advantage of automation to deliver truly exceptional experiences and products to their customers.

Reduce complexity and improve decision accuracy

Nicolas mentioned that at Hokodo, “The automation of our credit decisions has been a core value proposition for us since day one.” By taking an automated approach to its risk assessment, Hokodo has removed much of the complexity associated with offering products in multiple geographies.

By combining high-quality alternative data sources with internally developed risk models, Hokodo has created a highly accurate automated risk-scoring process for large parts of its customer segment.

Combine speed and human intervention

When thinking about automation, Philip from Tranch said their approach to automation “allows them to bring speed to a decision but also gives them the opportunity to have human intervention in the process when needed.”

Both Tranch and Hokodo tend to make risk-based views on which decisions are automated. They set thresholds for which loan values and customer types they automate decisions for and where manual reviews should be triggered. At Hokodo, for example, it comes down to the probability of default (PD) for a company and its size. If the PD of a company is low, Hokodo tends to feel more confident assigning automatically assessed limits.

Nicolas reiterated the importance of the manual and human aspects of their decision-making. By saving time on the automation of lower-risk decisions, Hokodo is able to spend the necessary resources on assessing applications with larger limits. This ensures customers across the board receive a fast, responsive experience.

Why alternative data sources are key to unlocking automation

Maik explained how Taktile is seeing strong patterns of B2B lenders using high-quality alternative data sources to automate risk assessment at different stages of a credit decision.

Open banking and accounting data sources are highly useful for automating decisions. Whether you integrate these into a fully automated decision flow or just use them to support manual reviews – they can significantly reduce the time it takes to get an accurate picture of a business's financial health and behavior.

What type of data source you leverage usually depends on the loan value and type of customer. Accounting data is often challenging to get predictive signals on young companies, but open banking data can be valuable. Maik said in SME lending, for example, “It really depends if your customer is the S or the M.”

Nicolas mentioned that Hokodo worked hard to find the best alternative data sources out there as there are nuances across every geography – “It’s a bit of a patchwork exercise to bring together sources that work really well for your use cases.”

Philip built on this by encouraging lenders to ask themselves, “How can I bring together data sources that give me a really accurate picture of what a borrower’s risk looks like?”

In Europe, Maik mentioned how PSD2 regulations make accessing open banking data quite affordable. Taktile is seeing lenders across Europe leveraging 2-3 open banking providers to build risk-scoring models for their customer segment.

How AI can benefit B2B decision-making

When it comes to leveraging AI in B2B lending decisions, Maik doubled down on the important distinction between machine learning models that have been trained using public data versus those trained on private data.

Chat GPT, for example, is based on a model trained on publicly available data on the internet. There is no customer default data publicly available on the internet for these models to be trained on, so they are not very useful in giving lenders an accurate probability of default for a borrower.

However, there are 2 ways Taktile has seen publicly trained models be incredibly powerful in B2B risk decisions:

1. Categorizing transactions in open banking data. In the B2B space, many data providers do not offer this capability. So it is helpful for lenders to leverage AI to automate the categorization of a borrower’s transactions.

2. Generating synthetic data. If you are a young company or just starting out in lending, you most likely do not have historical data to test the potential outcomes of your credit policy rules before you set them live. Using synthetic data sets generated by AI can be incredibly useful here.

Getting started with automation

Philp mentioned that much of automation can be thought about as removing customer friction – “it’s not about automating all of your operational processes. It’s about improving your customer experience. With even a little automation, such as the processing of documentation, you can get your customers from A to B much quicker”.

Nicolas also urges lenders to focus on the value proposition that automation brings to customers – especially if you’re an existing lender. “You have historical data; you have the knowledge. Leverage what you know and what people have learned from your manual processes to enhance the amount of automation in your processes.”

Maik also provided two key considerations for those new to automation:

1. Don’t overestimate the complexity or uniqueness of your situation. Many Taktile customers are surprised at how much potential there is with just a little automation. You just need to be ready to experiment with what decisions you automate.

2. Just get started, then figure out the rest. Even 1 percentage point of automation can free up valuable time for teams to assess the more complex decisions. In a time where profitability is paramount, achieving more with less has never been so important.

How modern decision engines make automation simple

Nicolas mentioned that automating decisions is no longer the challenge it used to be and that there are now providers out there that can help you do this well.

Maik explained how using a modern decision engine that is use-case agnostic is incredibly valuable for automating decisions: “The potential for automation in B2B lending is limitless.”

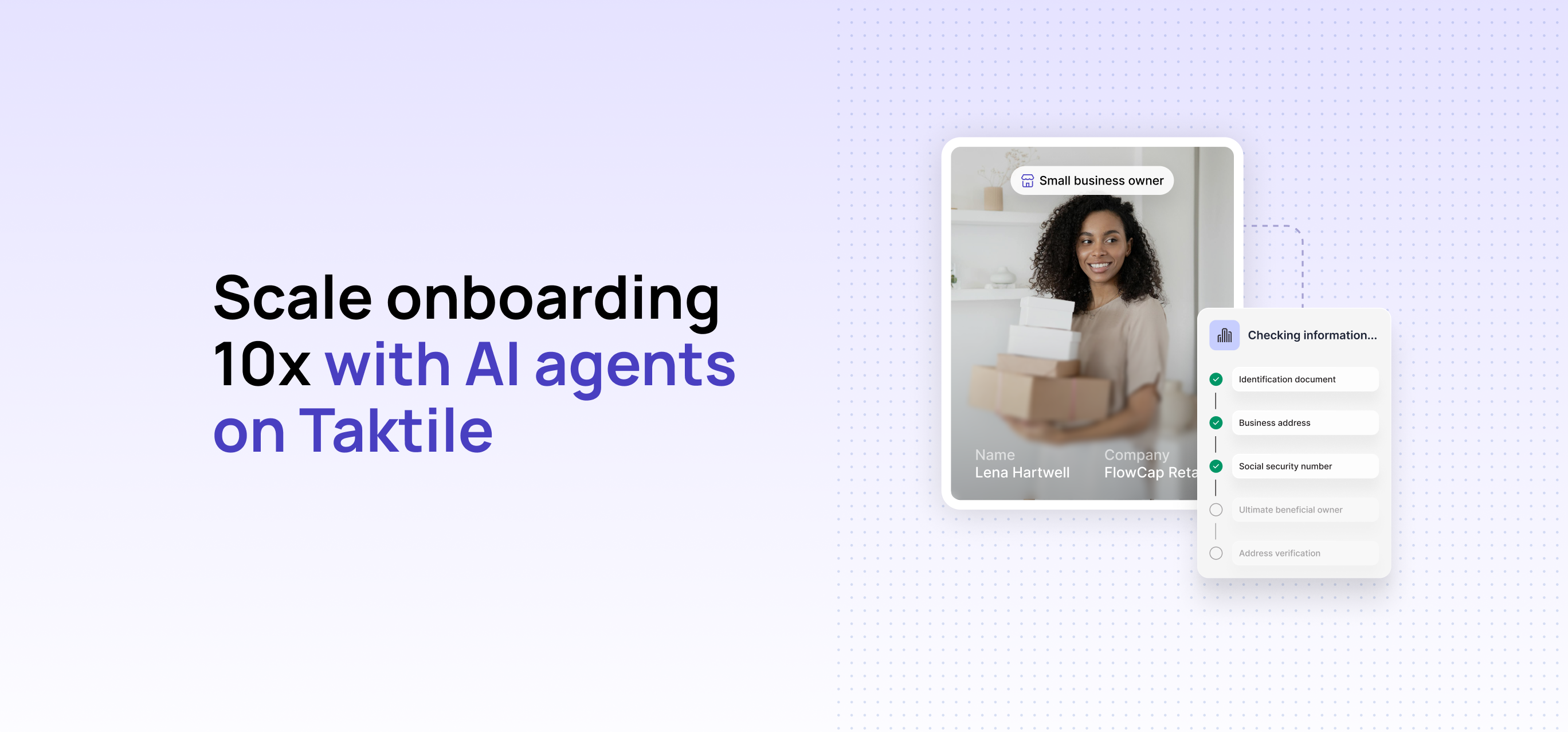

No matter their product or loan volume, lenders worldwide can use infrastructure providers like Taktile to build, experiment, and run automated credit decisions that always allow for a human in the loop.

On Taktile, the customer creates all the rules, policies, and models. Their teams are able to easily define their own limits and rules in a low-code user interface and iterate on them fast to figure out what the right amounts of automation are for each part of their customer segment.