When developing a lending product, one of your most important tasks is figuring out how to assess and price the risk of your customers. Doing this effectively enables you to approve the right customers, outprice your competition, and achieve positive unit economics.

Based on Taktile’s experience working with sophisticated lenders worldwide, this guide introduces you to the industry best practices used to assess and price risk in credit decisions – and the key trade-offs at each stage of the process.

Key takeaways

- Accurate risk assessment enables lenders to approve more of the right customers and identify market segments where they can offer better pricing than competitors.

- Structuring credit decisions into pre-selection, creditworthiness, affordability, and pricing stages helps manage cost, regulatory compliance, and customer friction.

- Early pre-selection reduces expensive downstream evaluations, but lenders should balance strict criteria against potential drop-offs.

- Using multiple data sources, including credit bureau, alternative, and open banking data, can improve default predictions and uncovers creditworthy customers with limited history.

- Affordability checks prevent over-indebting customers while providing insights to tailor loan sizes and pricing for higher approval rates.

- Differentiated pricing and limit-setting based on risk categories allow lenders to capture mispriced opportunities and optimize risk-adjusted returns.

Why is risk crucial to your lending decisions?

In most cases, lending requires you to give money to a customer without knowing with complete certainty that they can repay you – exposing you to financial risk. Therefore, it is important that you have processes in place to predict the likelihood of a customer not repaying a loan.

No matter the lending product, a lender’s goal is to come as close to the truth as possible in their risk predictions. The better you can predict risk, the better positioned you are to accept and price customers relative to their risk–and as a result, find pockets where you can offer more competitive pricing and increase revenue.

Lenders that struggle to do this well tend to have higher-than-expected loss rates and miss out on potential revenue by pricing customers too high relative to their risk.

How do lenders assess risk to make credit decisions?

One of the first steps in making credit decisions is to develop a comprehensive risk assessment framework known as a credit policy, which details general information about your lending product, as well as fraud and market risks. But most importantly, it defines how you predict the likelihood of a customer not repaying a loan – and takes steps to mitigate this problem.

To accurately assess risk, established lenders tend to build statistical models that consider the past behaviors (such as repayments and offer acceptance) of their customer base. However, as new lenders do not typically have access to historical customer data, they must instead rely on “expert-based” models with decision criteria based on industry best practices.

Although the variables lenders use to assess customer risk differ depending on their business model and customer segment, the process they follow to get to a credit decision tends to follow a similar structure.

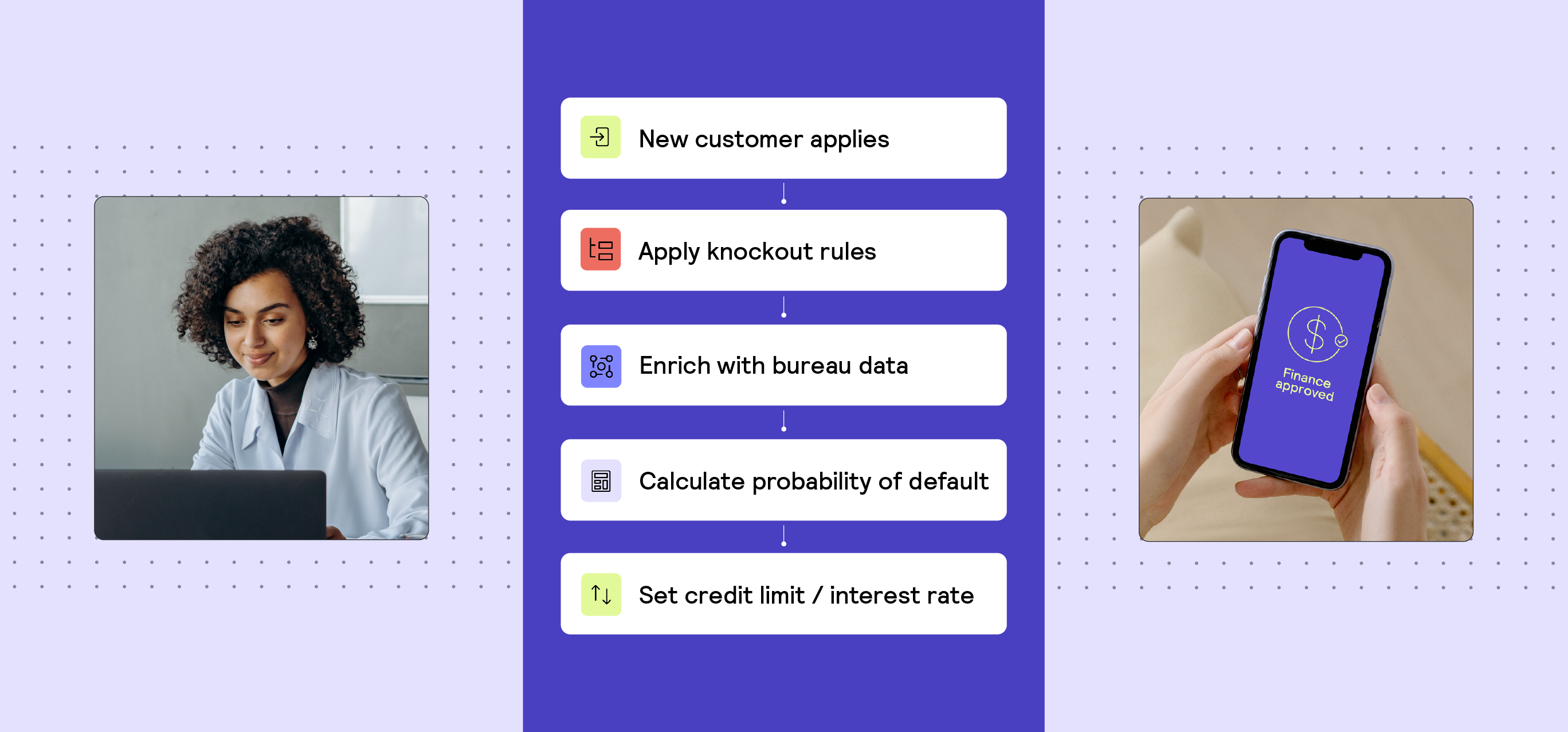

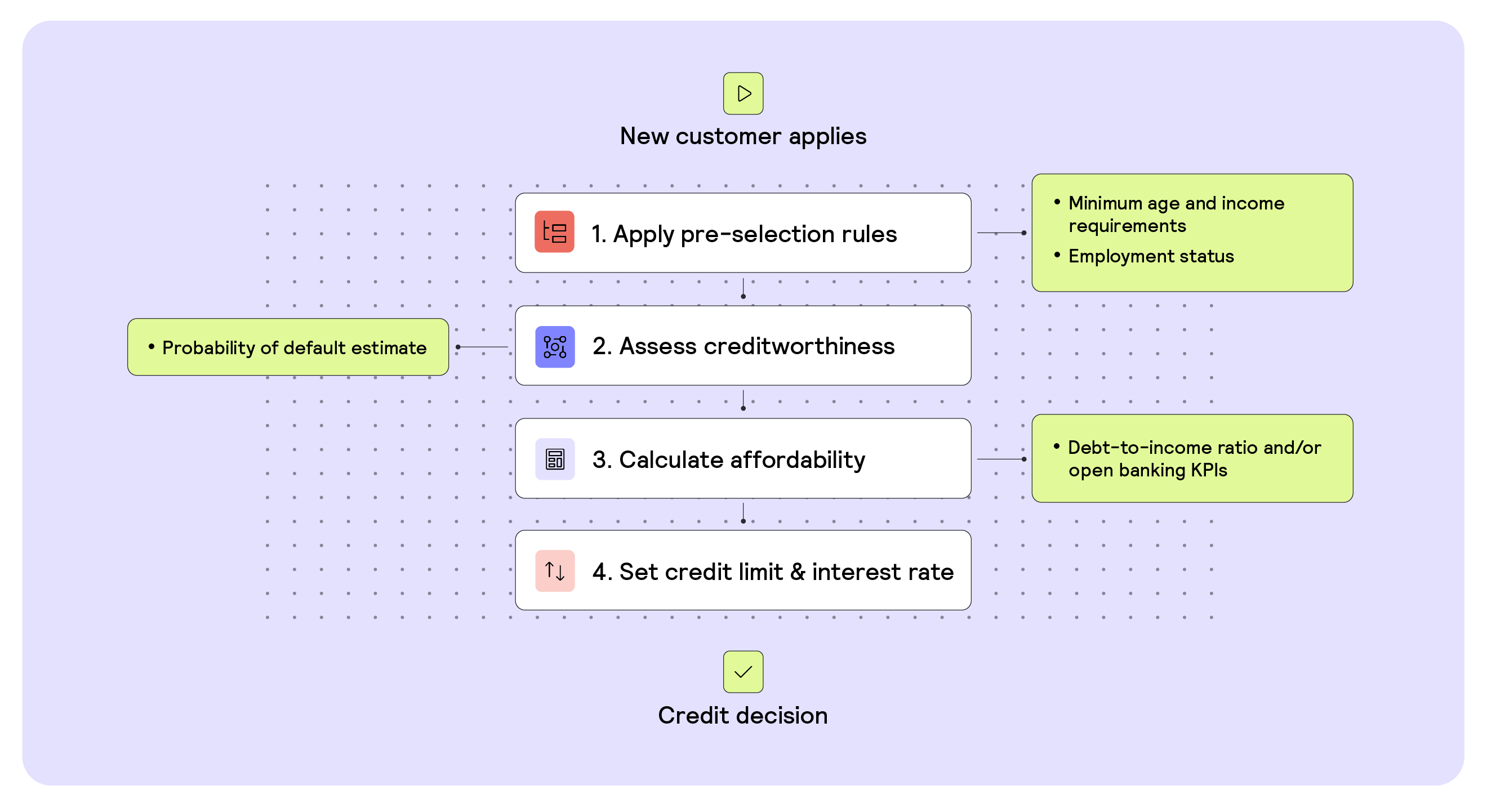

You can think about a credit decision as a funnel, where customers must satisfy specific criteria to move to the next stage. This process is typically broken down into 4 main steps:

1. Pre-selection

2. Creditworthiness assessment

3. Affordability calculation

4. Limit-setting and pricing

Before you get started: Regulatory considerations

Before you set your decision criteria, it is essential to understand the regulatory framework that applies to your lending product – as there may be requirements you have to satisfy that are specific to your offering, customer segment, and geography.

For example, high-value term loans typically require more comprehensive decision criteria than liquidity products like credit cards or overdrafts. Similarly, consumer loans tend to be more regulated than commercial loans.

Step 1: Pre-selection

The data you need to procure to adequately assess a customer’s repayment risk can get quite expensive (such as a credit bureau score). So lenders tend to set basic “pre-selection” criteria that customers must satisfy before moving them to the more costly stages of a credit decision.

The goal of this step is to exclude applicants that do not meet the most basic risk criteria and would, therefore, not pass later stages of the process.

How does pre-selection work?

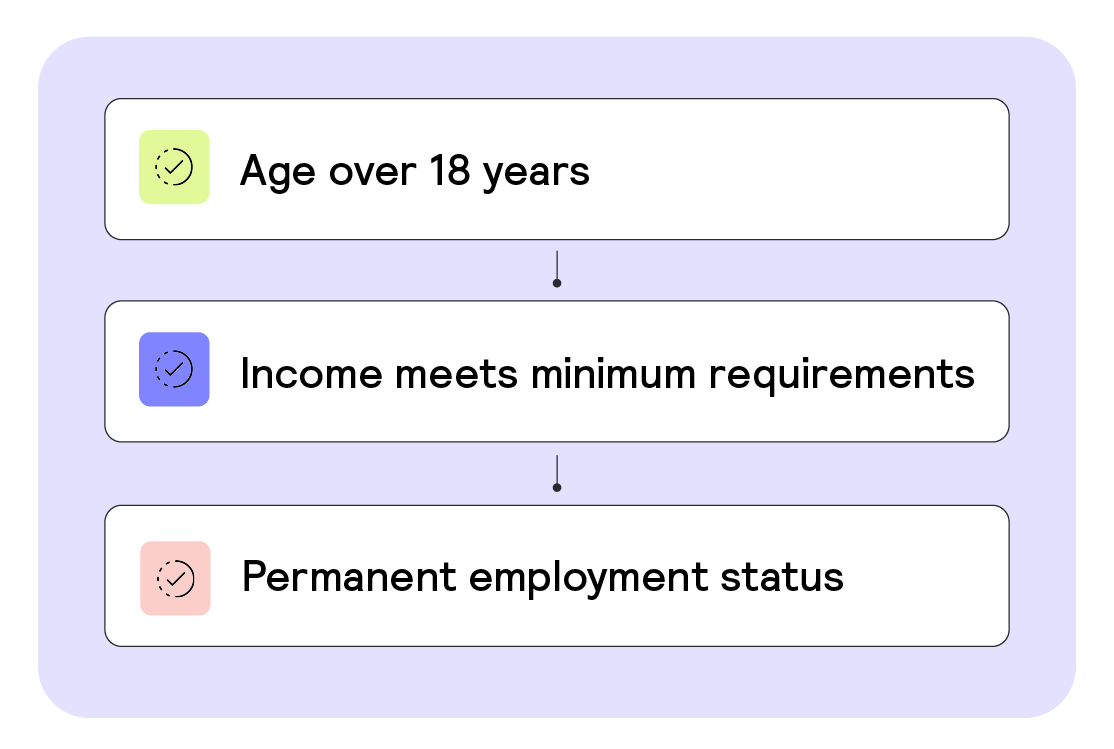

At the beginning of every application process, lenders typically ask for high-level information about an applicant, such as age, income, and employment status – then use this self-declared information to create “knock-out” rules.

What are typical acceptance criteria?

Typical knock-out rules define the minimum age, income, and employment status requirements an applicant must meet. For example, if an applicant declares they are under 18 years old, they are considered a minor and will be rejected from the application process straight away.

What are the trade-offs?

It can be tempting to ask applicants to declare a lot of information about themselves in the beginning so you can make an accurate pre-assessment of them. But by doing this, you can create friction for applicants, which may cause them to drop out of the application process. So when you set knock-out rules, it is important to consider the trade-off between pre-selection accuracy and customer drop-off rates.

Step 2: Creditworthiness assessment

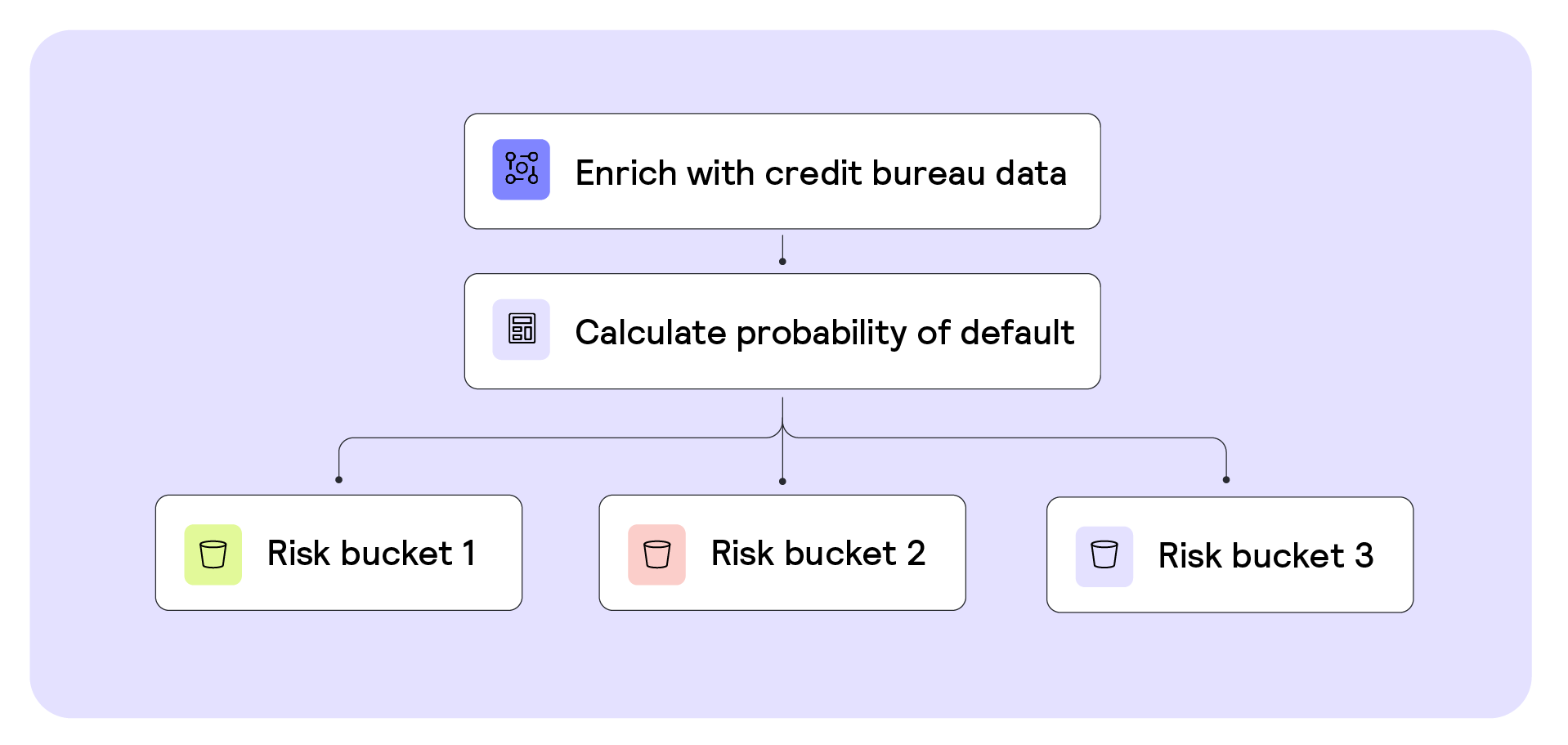

Once an applicant passes pre-selection, lenders typically assess whether or not they are suitable to receive a loan based on their previous financial behavior – also known as creditworthiness. To assess creditworthiness, lenders rely on a probability of default (PD) calculation, which predicts the likelihood that a customer will fail to repay a loan.

Not only is estimating a PD a regulatory requirement in most countries, but it is also one of the most significant indicators of repayment risk in the credit decision process. Therefore, the goal for lenders is to get an estimate for a PD that is as accurate as possible.

How do lenders predict the probability of default?

Lenders can use thousands of variables to estimate a PD, and generally, the best predictors come down to what is most suited to their lending product and customer segment.

In the consumer segment, for example, the most commonly used indicator of PD is a customer’s credit score. Provided by local credit bureaus, a credit score is calculated based on a customer’s credit history and known repayment behavior.

The fastest (and cheapest) way to access credit score data is by partnering with a third-party provider. CRS, for example, is one of the largest aggregators of credit bureau information in the United States, offering lenders quick access to consumer FICO scores from any relevant bureau.

Depending on the data aggregation methods and models credit bureaus use to calculate their scores, some third-party providers will be more suited to certain customer segments than others.

What happens if a customer has little to no credit history?

For segments where customers have little to no credit history (such as students, recent immigrants, or small businesses), most credit bureaus lack access to the data needed to generate accurate credit scores and assign low credit scores by default. Therefore, to offer lending products to these customers, lenders must rely on other indicators of financial behavior to generate a general risk score.

Take credit scoring in Germany, for example – a SCHUFA score is excellent for estimating the PD of adults over 25. But for customers younger than 25 (with less established credit histories), a CRIF credit score tends to be more accurate – as CRIF considers additional behavioral points from smartphone data.

Some lenders use particular credit bureaus that create risk scores based on repayment data from utility and telecommunication providers (such as Experian’s Clear Early Risk Score). Then others choose to calculate their own risk scores through alternative data sources.

Through open banking, lenders can gain detailed insight into a customer's previous financial behavior based on their transaction data. With SME customers, for example, lenders can leverage providers like Codat, which connect to a customer’s accounting data and provide “KPIs” about their previous repayment behavior. Learn more about using alternative data sources in credit decisions.

What are typical acceptance criteria?

The acceptance criteria lenders set based on a customer’s PD depend on their risk appetite, which is defined by multiple factors such as the interest rate they can charge, their business model, and their customer segment.

For example, if your goal is to grow quickly or lend to subprime customers, you may set very “loose” criteria that accept all customers that meet the basic regulatory requirements. However, if your goal is to achieve stable growth in a customer segment that is used to low interest rates, you may set stricter criteria that only accept lower-risk customers.

At a base level, lenders tend to set “hard” knock-out rules that reject customers with negative characteristics (such as insolvency) and those with very high PDs. Typically, customers with PDs of 25% or above are considered high-risk and subprime, and lenders with more conservative risk appetites or customer segments may choose to reject these customers off the bat.

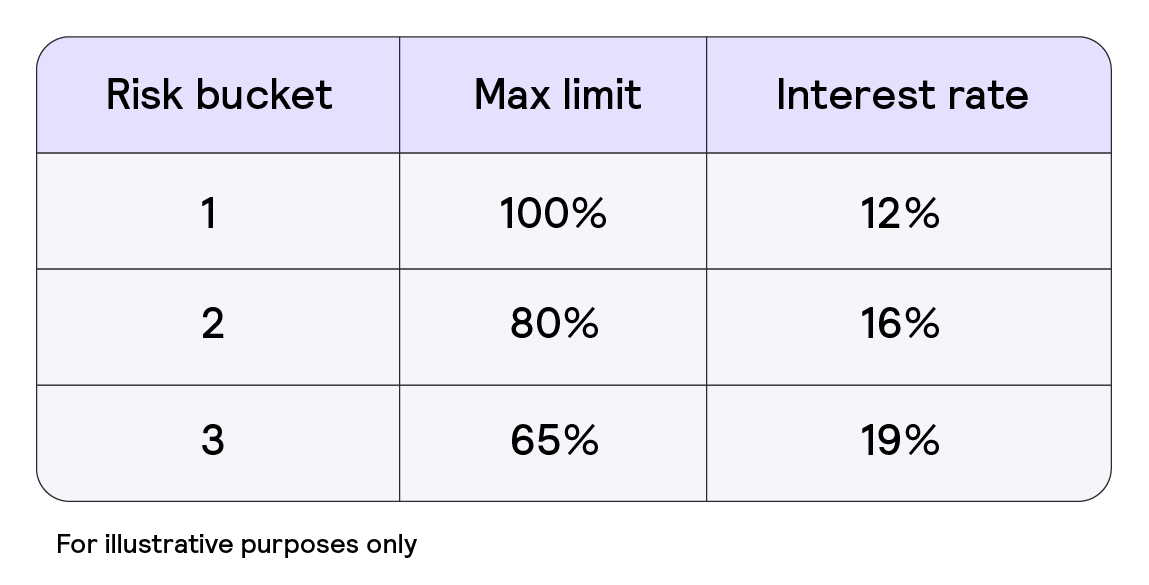

After lenders set initial knockout criteria, they decide which PDs they feel comfortable moving further through the process. Some even categorize their customers into what is known as “risk buckets” (by credit score, for example), which enable them to price customers more easily relative to their risk later in the process.

What are the trade-offs?

To increase the accuracy of their creditworthiness check, some lenders use multiple data sources (such as a credit report plus open banking) to predict a PD. However, they often have to make a trade-off between the accuracy of their risk assessment, cost per decision, and customer conversion.

While additional predictors increase accuracy, asking customers for their consent to pull data from multiple sources can introduce friction in their customer journey and result in them dropping out of the application process. Plus, data quickly becomes very costly, so you may have to make a trade-off between accuracy and the acquisition cost per customer.

Step 3: Affordability calculation

After assessing creditworthiness, lenders need to find out if a customer can afford to borrow the amount they have requested in their loan application. The decision criteria lenders set here serve two purposes. Firstly, it helps them determine the maximum loan amount a customer can afford to repay. And secondly, it proves to regulators that you take steps to not over indebt your customers.

How do lenders calculate affordability?

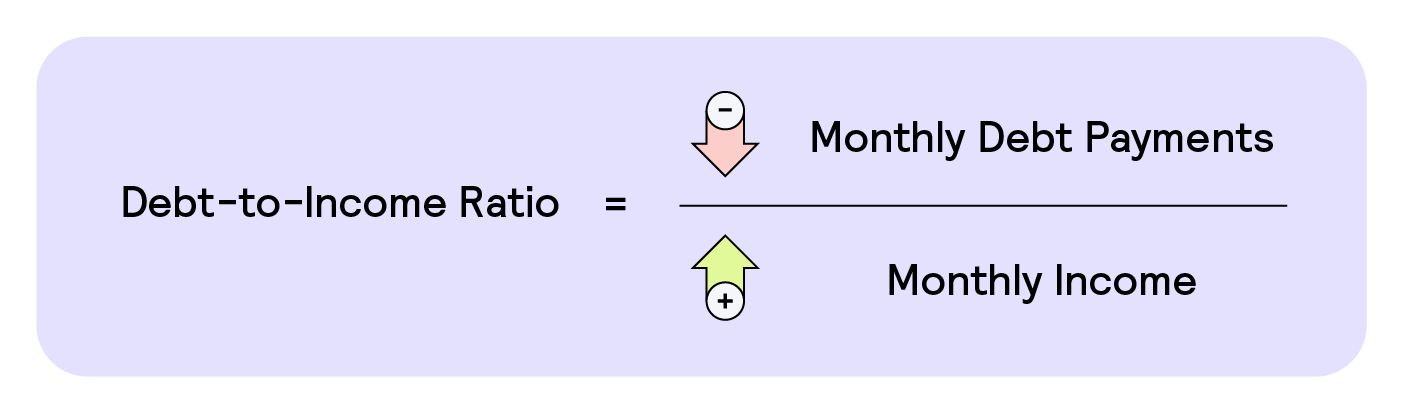

To assess a customer’s ability to repay a new loan, lenders often take a two-step approach. They start by calculating a debt-to-income (DTI) ratio, which gives them the percentage of a customer's monthly income that already goes to paying monthly debt repayments – such as credit card and mortgage repayments.

Then to calculate how much more debt a customer can afford to service monthly, lenders take into account other monthly household expenditures such as rent and utility bills.

While it is common to use credit bureau data in this step, you can also ask customers to provide their financial information in the application process or derive these insights directly from a customer’s financial data, such as bank account transactions.

The key advantage of having access to a customer's primary bank account data is being able to assess their income and outgoings in real-time to create an accurate financial picture. Not only does this help the accuracy of your affordability assessment, but it also helps you offer customers better pricing further in the decision process.

If you already offer other relevant financial products to your customers, such as debit cards, you may already have access to some of their transaction data. Most new lenders, however, choose to partner with third-party open banking providers. Plaid, for example, is the world’s largest open banking provider delivering lenders with raw transactional data and off-the-shelf KPIs that they can use to set their affordability criteria.

Although adding open banking KPIs allows you to be very granular in your affordability assessment – integrating them into your decision criteria is complex and time-consuming, so most new lenders rely on software providers to remove the burden. Taktile, for example, is a credit decision software that enables you to easily plug into all major data providers to launch your lending product quickly.

What are typical acceptance criteria?

The minimum affordability criteria lenders set based on a customer's DTI ratio (or similar KPIs derived from open banking data) depend on the benchmarks of their product and customer segment, and are often determined by regulators.

Depending on their risk appetite, some lenders may add additional buffers to minimum regulatory criteria that customers must satisfy to move further through the process.

What are the trade-offs?

As in the creditworthiness stage, open banking data can significantly improve the accuracy of your affordability assessments. Yet, it can also quickly increase your customer acquisition costs (if procured through a third-party provider).

Furthermore, asking for consent for open banking providers to connect to a customer’s bank account tends to be one of the major reasons customers drop out of the application process (up to 50%) – especially if the loan value is low.

Step 4: Limit-setting and pricing

Once lenders have assessed a customer’s creditworthiness and determined their affordability, they can price the customer’s loan.

The goal at this stage is to first determine the maximum amount you will lend on a product level – so what the maximum limit is for the “perfect customer”. And second, figure out the maximum amount you are willing to lend to a customer depending on their risk category.

How do lenders calculate pricing?

Similar to previous steps in the credit decision process, how lenders price their loans comes down to many factors. Their risk appetite, customer segment, and how much they can afford to give out to customers all affect their pricing strategy.

New lenders often start their pricing process by benchmarking their competition to see current loan volumes and pricing levels in their customer segments. Then they consider their own costs (such as price per customer acquisition or expected defaults) and determine how much margin they can add based on their product offering and their customer’s willingness to pay.

What are typical pricing criteria?

The criteria lenders set here depend on their pricing approach. Some lenders may simply set the same maximum loan amount and interest rate for every customer. However, to capture the highest possible risk-adjusted returns, most lenders differentiate these factors depending on a customer’s risk category. These categories could be based on the risk buckets you set in your creditworthiness assessment or just a customer's credit score.

This is where the accuracy of your PD estimates, and affordability calculations come into play. If you have highly accurate risk assessments of your customer segment, you can confidently identify the customers that are mispriced by the market (where other lenders charge interest that is too high given their actual PD). And by doing so, make more attractive offers than your competitors.

For example, customers that fall within higher risk categories may only be offered a percentage of the maximum loan amount plus a higher interest rate due to the increased risk the lender has to take on. On the other side of the spectrum, lower risk customers may be offered more competitive interest rates with higher maximum limits.

Conducting “what-if” analyses on different pricing scenarios can be helpful to determine the optimal pricing strategy for your segment. Using synthetic data, you can simulate potential outcomes on key metrics such as approval rates, loan amounts, and possible loss rates. State-of-the-art lenders use software providers like Taktile, which enable credit and risk teams to quickly create multiple versions of policies with different criteria to experiment with their risk and pricing strategies.

What are the key trade-offs?

The most significant trade-off when setting a pricing strategy tends to be between growth and profitability – as to capture more market share, lenders are often required to forgo some profits in order to offer more competitive pricing.

Ready to build your credit policy?

By following the general concepts outlined above, you should be well-positioned to create a highly effective credit policy that minimizes your loss rates, optimizes your approval rates, and gives you a competitive advantage in your customer segment.

If you want to get your product to market quickly, you can save time and money by using Taktile – the leading credit decision software provider used by sophisticated lenders worldwide. Leverage our battle-tested credit policy templates to get started in no time, or take advantage of our partnerships with some of the world's leading risk experts to help you build your own policy.

Disclaimer

This information provided in this article does not, and is not intended to constitute professional advice; instead, all information, content, and material are for general informational and educational purposes only. Accordingly, before taking any actions based upon such information, we encourage you to consult with the appropriate professionals.

Frequently Asked Questions (FAQs)

Q: What is credit risk assessment in lending?

A: Credit risk assessment is the process of predicting whether a borrower will repay a loan. By using data sources like credit bureau scores, open banking data, and affordability checks, lenders can reduce defaults and make more profitable lending decisions.

Q: How do lenders calculate creditworthiness?

A: Most lenders use probability of default (PD) models based on credit history, repayment behavior, or alternative data like open banking and utility payments. New lenders often start with expert-based credit policies before building statistical models.

Q: Why are affordability checks important in credit decisions?

A: Affordability checks, such as debt-to-income ratios and open banking insights, help lenders prevent over-indebtedness. They also ensure regulatory compliance and allow lenders to tailor loan amounts and interest rates to individual borrowers.

Q: What role does pricing play in credit risk management?

A: Differentiated pricing based on risk categories allows lenders to offer competitive interest rates to low-risk borrowers while protecting margins on higher-risk loans. This improves risk-adjusted returns and helps lenders win mispriced customers.

Q: How can Taktile help lenders improve risk assessment?

A: Taktile provides an intuitive, low-code Decision Platform that integrates multiple data sources, automates risk models, and enables rapid experimentation. Request a demo to see how Taktile’s AI Decision Platform can help you launch smarter credit policies, faster.